Corporate Tax Grouping and Group Relief in the UAE: When and How to Use Them

If you own multiple UAE entities, you are filing separate Corporate Tax returns for each one. That is the default. But the UAE Corporate Tax Law provides two mechanisms that can simplify compliance and reduce your overall tax bill: Tax Grouping and Group Relief.

Tax Grouping lets related companies file a single consolidated return. Group Relief lets one company’s losses offset another company’s profits. Both require careful structuring to get right, and both carry risks that most advisors gloss over.

Quick answers

- What is a Tax Group? Two or more UAE resident companies that elect to be treated as a single taxpayer for Corporate Tax purposes, filing one consolidated return.

- What is Group Relief? A mechanism that allows one group company to transfer current-year tax losses to another group company, without forming a Tax Group.

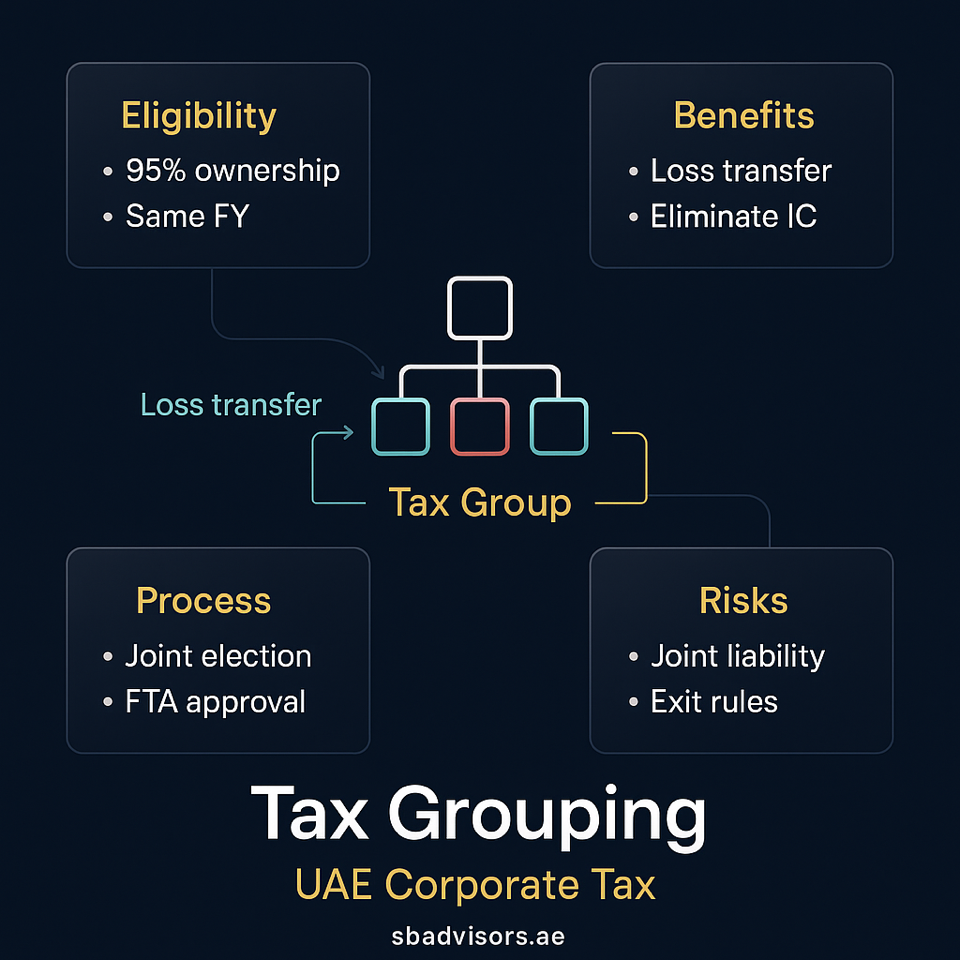

- Who qualifies? The parent must own at least 95% of the subsidiary (directly or indirectly) for Tax Grouping. Group Relief requires 75% common ownership.

- Can free zone companies be in a Tax Group? Yes, but a QFZP cannot be the parent or a member of a Tax Group with a non-free zone entity if it wants to maintain the 0% rate on qualifying income.

- What is the main risk? Joint and several liability. In a Tax Group, every member is liable for the entire group’s Corporate Tax obligation.

- Is it worth it? Depends on your structure. If one entity is profitable and another has losses, Group Relief can save real tax. If your entities are all profitable, the compliance simplification of a Tax Group may not justify the joint liability risk.

Tax Grouping

How it works

A Tax Group is formed when a parent company and one or more subsidiaries elect to be treated as a single taxable person. The group files one Corporate Tax return, and intra-group transactions are eliminated for tax purposes.

This means:

- Revenue and expenses between group members are ignored.

- Profits and losses of all members are combined into a single taxable income figure.

- The AED 375,000 zero-rate threshold applies once to the group, not to each member separately.

- One return is filed instead of multiple returns.

Eligibility requirements

To form a Tax Group, the following conditions must be met:

- UAE residency: Both the parent and subsidiary must be UAE resident persons (i.e., incorporated in the UAE or effectively managed and controlled from the UAE).

- 95% ownership: The parent must hold at least 95% of the share capital and 95% of voting rights of the subsidiary, directly or indirectly through other group members.

- Same financial year: All group members must have the same financial year-end.

- Same accounting standards: All members must prepare financial statements using the same accounting framework (IFRS, IFRS for SMEs, etc.).

- Not a QFZP (for mixed groups): A Qualifying Free Zone Person cannot be part of a Tax Group that includes non-free zone entities if it wants to maintain the 0% rate on qualifying income. Two QFZPs can form a group among themselves.

- Not an exempt person: Government entities and other exempt persons cannot be group members.

Application process

- The parent company submits a Tax Group application to the FTA through EmaraTax.

- The application must include details of all proposed members, ownership structure, financial year alignment, and confirmation that eligibility conditions are met.

- The FTA reviews and approves (or rejects) the application.

- Once approved, the Tax Group takes effect from the beginning of the tax period specified in the application.

Intra-group transaction elimination

Once a Tax Group is formed, transactions between members are eliminated. This includes:

- Sales of goods or services between group companies.

- Management fees and intercompany charges.

- Interest on intercompany loans.

- Asset transfers between members.

This eliminates the need for transfer pricing documentation on these specific transactions (since they no longer exist for tax purposes), though the arm’s length principle still applies to transactions with entities outside the group.

Joint and several liability

This is the most significant risk. Every member of a Tax Group is jointly and severally liable for the entire group’s Corporate Tax obligation. If the parent cannot pay, the FTA can pursue any subsidiary for the full amount.

Consider this carefully if:

- One group member has high-risk operations or volatile income.

- You plan to sell a subsidiary (the buyer inherits group-period tax liabilities).

- One member is in a different regulatory environment (e.g., a DIFC entity grouped with a mainland entity).

Group Relief (Loss Transfer)

How it works

Group Relief allows a company with a current-year tax loss to transfer that loss to another group company that has taxable income, reducing the recipient’s Corporate Tax liability. Unlike a Tax Group, each company continues to file its own return.

Eligibility requirements

- 75% common ownership: The transferor and transferee must be at least 75% owned (directly or indirectly) by the same ultimate parent. Note this is a lower threshold than the 95% required for Tax Grouping.

- UAE residency: Both companies must be UAE tax residents.

- Same financial year: Both must have the same financial year-end.

- Not a QFZP: Losses from a QFZP’s qualifying activities cannot be transferred to a non-QFZP entity through Group Relief.

- Current-year losses only: Only losses incurred in the current tax period can be transferred. Carried-forward losses from prior periods cannot be transferred via Group Relief.

How to apply

- Both the transferor (loss-making company) and the transferee (profitable company) must submit a joint election to the FTA.

- The election is made as part of the Corporate Tax return filing for the relevant tax period.

- The amount of loss transferred is specified in the election.

- The transferor’s taxable income is increased by the loss transferred (effectively reversing the deduction).

- The transferee’s taxable income is decreased by the loss received.

Practical example

Company A (subsidiary) has a tax loss of AED 500,000. Company B (subsidiary) has taxable income of AED 2,000,000. Both are 100% owned by a UAE holding company.

Without Group Relief:

- Company A: AED 0 tax (loss carried forward).

- Company B: AED 2,000,000 - AED 375,000 = AED 1,625,000 x 9% = AED 146,250 tax.

- Total group tax: AED 146,250.

With Group Relief (transferring AED 500,000 from A to B):

- Company A: AED 0 tax (loss transferred, nothing to carry forward).

- Company B: AED 2,000,000 - AED 500,000 = AED 1,500,000. After threshold: AED 1,125,000 x 9% = AED 101,250 tax.

- Total group tax: AED 101,250.

- Saving: AED 45,000.

Tax Grouping vs. Group Relief: Which to Choose?

| Feature | Tax Grouping | Group Relief |

|---|---|---|

| Ownership threshold | 95% | 75% |

| Filing | One consolidated return | Separate returns per entity |

| Intra-group eliminations | Yes (automatic) | No |

| Loss utilisation | Automatic (consolidated P&L) | Elective (current-year only) |

| AED 375,000 threshold | Applied once to the group | Applied per entity |

| Joint liability | Yes (all members) | No |

| Transfer pricing on interco | Eliminated within group | Still required |

| Complexity | Higher setup, simpler ongoing | Lower setup, per-period election |

When Tax Grouping makes sense:

- Large groups with significant intercompany transactions (eliminates TP complexity).

- Groups where one entity consistently has losses (automatic offset).

- Groups that want simplified compliance (one return instead of many).

When Group Relief is better:

- Ownership is between 75% and 95% (Tax Grouping is not available).

- You want to preserve separate liability for each entity.

- Loss transfers are occasional, not every year.

- You may sell a subsidiary and do not want it carrying group tax liabilities.

Leaving a Tax Group

A member can leave a Tax Group if:

- Ownership drops below 95%.

- The member is sold to an external party.

- The FTA revokes the group status due to non-compliance.

- The parent voluntarily deregisters the member.

When a member leaves, any assets transferred within the group at tax-neutral values may trigger a clawback. The FTA can assess Corporate Tax on the deferred gains from prior intra-group transfers. This catch is easy to miss during M&A transactions and should be modelled before any group member disposal.

Frequently Asked Questions

Can a sole establishment be part of a Tax Group? No. Tax Grouping requires juridical persons (companies). Sole establishments and natural persons conducting business cannot form or join a Tax Group.

Does the AED 375,000 zero-rate band apply once or per member? In a Tax Group, it applies once to the consolidated taxable income. This is a disadvantage if each member independently earns under AED 375,000, as they would individually pay zero tax without grouping.

Can I transfer losses from a free zone company to a mainland company? Only if the free zone company is not a QFZP or the losses relate to non-qualifying income. Losses from qualifying activities of a QFZP cannot be transferred to a non-QFZP through Group Relief.

What happens to carried-forward losses when joining a Tax Group? Pre-grouping losses of a subsidiary remain ring-fenced. They can only be used against the future profits of that specific subsidiary within the group, not against the consolidated group income.

Can a holding company with no operations be the parent of a Tax Group? Yes, provided it is a UAE resident juridical person and meets the ownership requirements. Many UAE groups use a holding company as the Tax Group parent.

Is there a deadline to elect for Tax Grouping? The application should be submitted before the start of the tax period for which the group is to take effect, or within the timeframe specified by the FTA. Late applications may result in the grouping only taking effect from the following period.

Can I undo a Tax Group election? Yes, but it requires FTA approval and may trigger clawback provisions on prior intra-group transfers.

How Success Business Advisors can help

We model whether Tax Grouping or Group Relief produces a better outcome for your specific structure, prepare the FTA applications, manage the consolidated return, and flag clawback risks before you restructure. Book a consultation and we will review your group structure in 30 minutes.

Ready to take the next step?

Schedule an Appointment WHO WE WORK WITH

WHO WE WORK WITH